The collapse of the Terra (LUNA) ecosystem gave more weight to the rumors of Tether (USDT)’s fragility. We dive into the likelihood of a USDT de-peg and map out its possible consequences.

TL;DR

- The collapse of UST ushered a flight to collateralized stablecoins

- Based on current data, USDT is unlikely to experience a permanent de-peg

- A permanent USDT/USD de-peg would be less impactful to the crypto ecosystem than UST’s

The flight to collateralized stablecoins

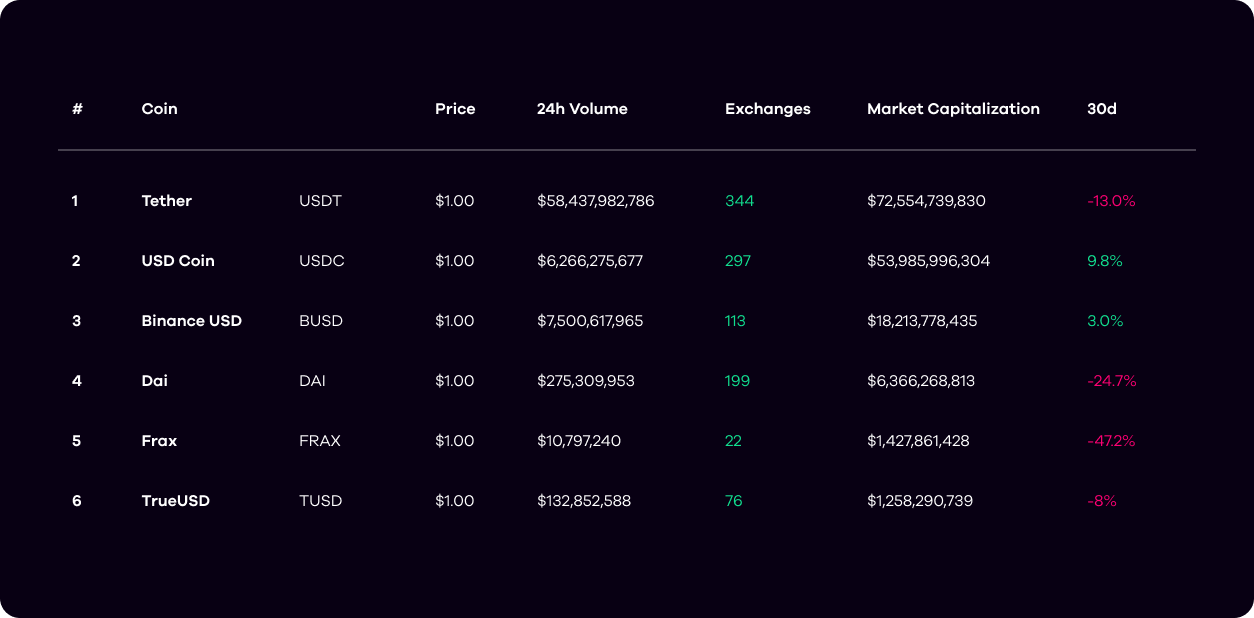

After what happened to Terra mid-May, we looked for destabilization risks among other systemically important stablecoins. We started by looking only at the tokens with a market cap greater than $1B. Out of these seven tokens, four are fully collateralized stablecoins. They’re also the three biggest stablecoins in terms of market capitalization. They are deemed fully collateralized/backed because their peg to the USD is supposed to be 100% backed by reserves: If all users wanted to redeem their tokens at the same time, they should expect to do so without loss.

Since the UST crash, investors have unsurprisingly fled away from crypto-collateralized or algorithmically backed stablecoins towards fully backed ones. Over the 30 days ending June 1, 2022, the circulating supplies of DAI, MIM, FRAX, and UST have decreased by 29%, 85%, 47%, and 95%, respectively. In the meantime, fully collateralized stablecoins like USD Coin (USDC) and Binance USD (BUSD) have seen their circulating supply increase by 9.8% and 3% respectively.

But that’s not the whole story. Two other large stablecoins labeling themselves as fully collateralized have faced headwinds. During the same period, the circulating supplies of True USD (TUSD) and Tether’s USDT – the largest stablecoin in the world – have decreased by 8.5% and 13%, respectively. You can see this movement in the chart below:

Source: CoinGecko as of June 1, 2022

Why would investors be running away from supposedly risk-free assets during a time of market stress? Simple: They have concerns over the quality of these assets’ collateral. USDC reports its reserves monthly, is audited by a top-5 accounting firm in the U.S. with thousands of employees, and is currently holding all of its balance sheet in cash and short duration U.S. Treasuries, as the graph above shows:

In the case of Tether’s holdings, the market is much less confident. It’s precisely because of speculation regarding its reserves that USDT was the only stablecoin to experience a notable break from its peg in the wake of the UST crash. Over the period from May 11 to May 12, USDT has traded below its $1 peg to a low of $0.9565, before recovering over the next 36 hours to trade at a slight discount of $0.998. During this time, USDC, BUSD, and DAI traded at premiums of 1-2% above the peg as investors moved towards assets they perceived as less risky.

The market’s skepticism towards USDT’s reserves has amplified since the $41M fine Tether received in October 2021 by the U.S. government for misrepresenting the nature of its reserves. Given that USDT is the only fully backed stablecoin to have experienced a de-peg recently, and because of its importance to the crypto ecosystem, investors increasingly speculate over its likelihood to de-peg permanently.

Probabilities of a permanent USDT/USD de-peg

First, by permanent de-peg we mean a de-peg so severe the asset cannot regain its peg – like the one UST experienced a few weeks ago. Since USDT is deemed fully backed, the likelihood of a permanent de-peg heavily depends on the nature of its reserves.

Now, although it’s possible that the amount of Tether’s reserves communicates may be inaccurate, or that their credit quality may be overstated, we do believe that a significant portion of their liabilities are backed by real, liquid assets. Based on Tether’s most recent attestation report of their reserves, which we’ve consolidated in the graphic below, over 60% of the assets held on the balance sheet as of 03/31/2022 are in safe, liquid assets. The other ~39% of the balance sheet is invested in assets we deem to be lower in quality and/or liquidity. Thus, in a scenario where all USDT holders sought USD liquidity, we would expect Tether to return at least 61% of assets back in short order. This means that for every 1 USDT in circulation, we expect Tether would be able to pay back at least $0.61 if all minted tokens were redeemed for USD.

While USDT does play an important role in the crypto ecosystem, it is not directly linked to the performance of another digital asset like UST was connected to LUNA. In other words, there is no asset that would experience a 1:1 decline in market capitalization as USDT de-pegged so there would be no additional direct losses.

Since the date of the attestation report, USDT assets have fallen from $82.4B to ~$73.3B today. Assuming the above 61%/39% ratio still holds true, a complete USDT liquidation event would result in explicit losses of ~$28.6B (39% x $72.3B). Although the scenario laid out above uses highly conservative assumptions, the direct losses from a USDT collapse would be significantly lower than those caused by UST ($28B vs. $46B).

Consequences of a possible Tether depeg

What about indirect losses, or losses caused by ripple effects? We believe these are also likely to be lower than those caused by UST due to the limited use of USDT as lending collateral. Compared to UST, USDT is lightly used in DeFi protocols at $3B compared to ~$12B for UST prior to the de-peg. The more heavily a stablecoin is utilized as collateral in DeFi protocols the greater the amount of forced liquidations that will result from a de-pegging event. Additionally, because stablecoin TVL is directly correlated to DeFi protocols market cap, the larger the TVL, the greater the effect a de-peg will have on the DeFi market capitalization.

In the wake of the UST crash, there was an overall decline of ~$45B in global DeFi market cap from May 6 to May 21, implying a ~3.5x ratio of losses to DeFi deposits. We can use this ratio of losses to DeFi deposits as a rough approximation for the damage a USDT de-peg would cause to the global DeFi sector. Since there is ~$3B of USDT located in DeFi protocols across Ethereum, Tron, Solana, BSC, and others, we would expect ~$10.5B of DeFi-related losses stemming from a USDT de-peg.

As for how much overall losses the overall crypto market would experience, we anticipate a similar ratio of UST-driven losses to USDT-driven losses. We’ve forecasted the expected losses for USDT using what we call “Implicit to Explicit Loss Ratio” below, and compare it to what was experienced in the wake of the UST collapse.

We acknowledge that our analysis does not focus on USDT’s importance to the off-chain crypto industry (i.e. centralized exchanges). A majority of BTC transactions are done using USDT, and USDT is the most-traded digital asset and most-used quote currency for all non-US based exchanges. Although a de-peg is very likely to cause a short-term liquidity crunch and volatile price swings like what happened from May 11 – 12 when BTC fell 15% on the back of Tether falling to $0.95, we believe over the medium and long term that the damage to the crypto ecosystem will be less than what was experienced due to UST.

To learn more about what happened to LUNA and UST, read our Okcoin Insights blog.